The Complete UK Payroll Guide for Small Businesses and Startups

Running payroll for your small business doesn’t have to be overwhelming. Whether you’re a startup hiring your first employee or a growing company expanding your team, understanding UK payroll requirements is essential for staying compliant and avoiding costly penalties.

This guide covers the fundamentals of UK payroll, from PAYE basics to your ongoing obligations as an employer.

Understanding PAYE: The Foundation of UK Payroll

What is PAYE?

Pay As You Earn (PAYE) is HMRC’s system for collecting income tax and National Insurance from employees. Employers must calculate wages, deduct the correct amounts, and pay these to HMRC on time. Mistakes or delays can result in HMRC penalties, cash flow issues, and a loss of employee trust.

Key PAYE Components

Income Tax: Calculated based on the employee’s tax code and earnings. Most employees have a tax code starting with numbers (like 1257L) which determines their tax-free personal allowance.

National Insurance: Both employees and employers pay National Insurance contributions. The rates depend on earnings levels and are calculated using NI categories (typically Category A for most employees).

Student Loan Repayments: If an employee has a student loan, you may need to deduct repayments based on their earnings and repayment plan type.

Getting Started with PAYE

Before running your first payroll:

Real Time Information (RTI): Staying Connected with HMRC

What is RTI?

Under RTI employers are required to report payroll information to HMRC every time they pay employees, not just at year-end. This happens through Full Payment Submissions (FPS) sent electronically.

RTI Submission Requirements

On or before payday: You must send an FPS to HMRC with details of who’s been paid, their gross pay, deductions (income tax, National Insurance, student loans, etc.), and net pay.

Nil returns: If you don’t pay anyone in a pay period but are still an active employer, you must submit an Employer Payment Summary (EPS) to notify HMRC.

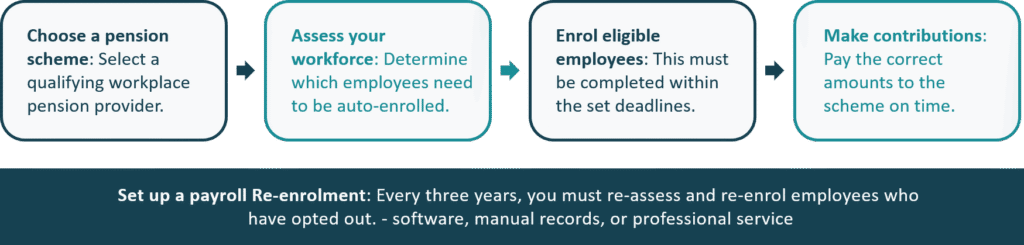

Auto-Enrolment Pensions: Your Legal Obligations

Understanding Auto-Enrolment

If you employ at least one person, you have duties under auto-enrolment legislation. This requires you to automatically enrol eligible employees into a workplace pension scheme and make contributions.

Who Must Be Auto-Enrolled?

Employees must be auto-enrolled if they:

- Are aged between 22 and State Pension age

- Earn more than £10,000 per year

- Work in the UK

Auto-Enrolment Process

Auto-enrolment can be complex, especially for businesses with fluctuating workforce or irregular pay patterns.

Managing Different Types of Employees

Payroll rules differ for full-time, part-time, and director employees. Knowing these differences ensures accurate pay and compliance.

Statutory Payments: Your Legal Obligations

As an employer, you must provide statutory payments like sick pay, maternity pay, and paternity pay when employees take time off. Each has specific eligibility rules, rates, and repayment processes.

Year-End Responsibilities

P60s for All Employees

By 31st May each year, provide all employees (including those who left during the year if they were employed on 5th April) with a P60 showing their total pay and deductions for the tax year.

P11D for Benefits in Kind

If you provide employees with benefits like company cars, private medical insurance, or other perks, you must report these on P11D forms by 6th July.

Final RTI Submissions

Ensure your final FPS of the tax year is marked as such and includes any corrections to earlier submissions.

Payroll: DIY vs Outsourcing

Running payroll yourself can save money but takes time, increases the risk of errors, and means you must keep up with changing legislation. Outsourcing to a professional service ensures accuracy, compliance and frees up your time to focus on growing your business.

At KT Accounts, we handle everything from RTI submissions to auto enrolment, year end processing and ongoing compliance, giving you peace of mind and protecting you from costly HMRC penalties.

Conclusion

Managing payroll effectively is essential for any UK business with employees. While the rules around PAYE, RTI and auto-enrolment can seem complex, understanding the basics helps you stay compliant and avoid costly mistakes. Payroll is not just about ticking HMRC boxes – it’s about taking care of your team by ensuring they are paid accurately and on time.

For many small businesses, outsourcing payroll provides the perfect balance of expertise, compliance and value. At KT Accounts, we deliver accurate, professional payroll management so you can focus on growing your business with complete confidence your obligations are met.